What to Do When You Run Out of Cash and Have Bills to Pay

Learn how to regain control of your finances in tough times.

-

Fitz Villafuerte

Fitz Villafuerte

-

Manage Money

Manage Money

-

Published March 14

Published March 14

Table Of Contents

So, you’ve run out of cash. Now what?

First off, take a deep breath. We’ve all been there—staring at the bills piling up and realizing that your bank account balance isn’t going to cut it. It’s a stressful moment, no doubt, but the key here is to act quickly and strategically. This isn’t the end of the world; with a bit of planning, you can navigate through this rough financial patch.

Step 1: Get Real About Your Financial Situation

Before you do anything, you need to get a clear picture of where you stand. I know it’s tempting to bury your head in the sand but trust me—knowing exactly what you’re dealing with is half the battle.

Start by listing out all your current assets. Do you have any cash tucked away in a savings account? Any upcoming income that hasn’t hit your account yet? Maybe you could even consider selling some valuables. Put it all down on paper (or a spreadsheet, if that’s more your vibe).

Next, it’s time to prioritize. Not all bills are created equal. Your rent, utilities, and groceries are non-negotiable—those are the essentials.

Things like subscription services, dining out, or that gym membership you haven’t used in weeks? Those can wait. Identify what absolutely needs to be paid and what can be postponed.

Step 2: Find Some Quick Cash

Alright, now that you’ve got a handle on what needs to be paid, let’s talk about where to find some quick cash. You’ve got options:

Borrowing

This isn’t about maxing out your credit cards. Think about reaching out to family or friends—just make sure you’re upfront about when you can pay them back. If you’re considering a loan, be sure to do your homework. Government loans are usually your best option.

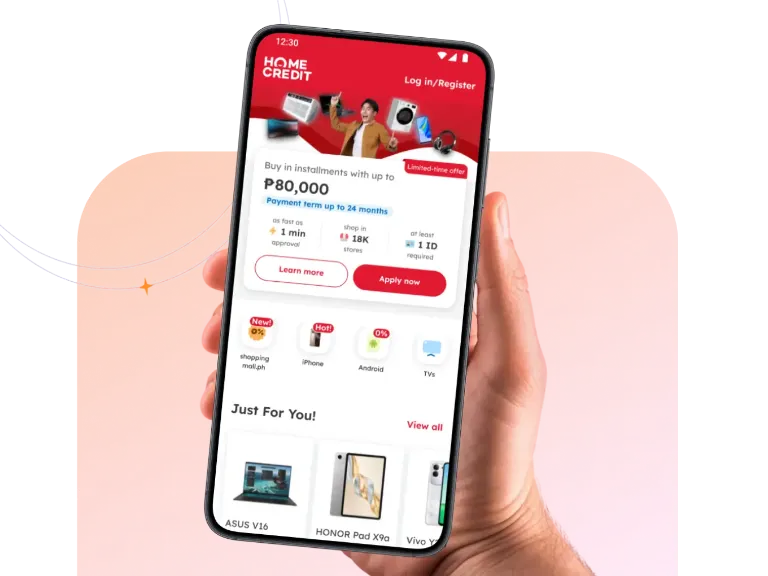

Need a Reliable Loan Option?

If you plan to borrow, you can trust providers like Home Credit. They can help you manage your finances with flexible cash loans and credit options like HCQWARTA or Home Credit Card. Check the app for available offers!

Selling Stuff

Got a bike collecting dust? An old phone you don’t use? Liquidating non-essential items can give you a cash boost. You can sell on social media like Facebook Marketplace or even try a garage sale. Just be mindful of what you’re willing to part with.

Gig Economy

These days, there’s a gig for almost everything. Whether it’s freelancing, ridesharing, or delivering groceries, there’s money to be made on the side. It might not be glamorous, but it can help you bridge the gap.

Step 3: Negotiate Like a Pro

Now, it’s time to put those negotiation skills to work. Most people don’t realize that you can often negotiate with your creditors and service providers. The key? Communication.

Call Your Creditors

Pick up the phone and explain your situation. Most companies would rather work with you than see you default. Ask about payment plans, deferments, or any temporary relief they can offer.

Talk to Your Landlord or Utility Providers

This can be intimidating, but many landlords and some utility companies are willing to work out a payment plan, especially if you’ve been a reliable tenant or customer. Don’t wait until you’re behind to have this conversation—get ahead of it.

Consider Debt Consolidation

If you’ve got multiple debts, consolidating them might make sense. It can simplify your payments and sometimes lower your interest rates. Just be sure to understand the terms before jumping in.

Step 4: Seek Out Financial Assistance

If you’re still feeling the pinch after exploring the above options, don’t be afraid to seek out help. There’s no shame in using the resources available to you:

Government and Non-Profit Programs

Depending on where you live, you might be eligible for emergency assistance like meal allowances, social welfare assistance, or unemployment benefits. These programs are there for a reason—don’t hesitate to apply if you need them.

Community Resources

Local charities, food banks, and even religious organizations often provide help to those in need. It might take a little research, but these resources can make a big difference when you’re in a tough spot.

Step 5: Make a Long-Term Plan

Once you’ve weathered the immediate storm, it’s time to think long-term. How can you prevent this from happening again?

Budget Like a Boss

Budgeting doesn’t have to be a boring chore. Think of it as giving yourself the freedom to spend on what really matters. There are tons of apps and do-it-yourself strategies that are fun and effective. The goal here is to track your spending and find areas where you can cut back.

Build an Emergency Fund

I know, easier said than done, but even stashing away a small amount each month can add up. Aim for at least P10,000 to start—it’s not a lot, but it’s enough to cover most small emergencies. Over time, work towards saving three to six months’ worth of living expenses.

Up Your Financial Literacy

The more you know, the better equipped you’ll be to handle financial challenges in the future. Whether it’s reading books, watching videos, attending a seminar, or just following a few financial content creators, there’s always something new to learn.

You’ve Got This

Running out of cash is tough, but it’s not the end of the road. By staying calm, making a plan, and reaching out for help when you need it, you can get through this and come out stronger on the other side.

Financial setbacks happen, but they don’t define you. Take it one step at a time, and remember—you’re more resilient than you think.

Manage your finances with Home Credit!

Don’t let expenses weigh you down. Home Credit Philippines offers various options such affordable product installment plans to help you purchase essentials, cash loans for major milestones, and even Home Credit Card or HCQWARTA for hassle-free transactions.

Plus, the Loan Extra Care add-on can give you the flexibility to adjust your payments during tough times. Check the Home Credit app for your options!

About the author: Fitz Gerard Villafuerte is a civil engineer who decided to quit the corporate world back in 2003 to pursue freelancing and entrepreneurship. You can read more financial tips on his blog, Ready To Be Rich, which has won several awards including the Best Business and Finance Blog at the Philippine Blog Awards. He is recognized by Moneysense Magazine as among the Top 12 Most Influential People in Personal Finance in the Philippines. He is an author; an online content creator; a Registered Financial Planner; a resource guest for various television and radio programs; and a corporate speaker and trainer for several socio-civic organizations in the country. Lastly, he is the President of Wealth Arki, Inc., an investment consultancy, and financial planning firm that helps Filipino families achieve their financial goals.

.webp)